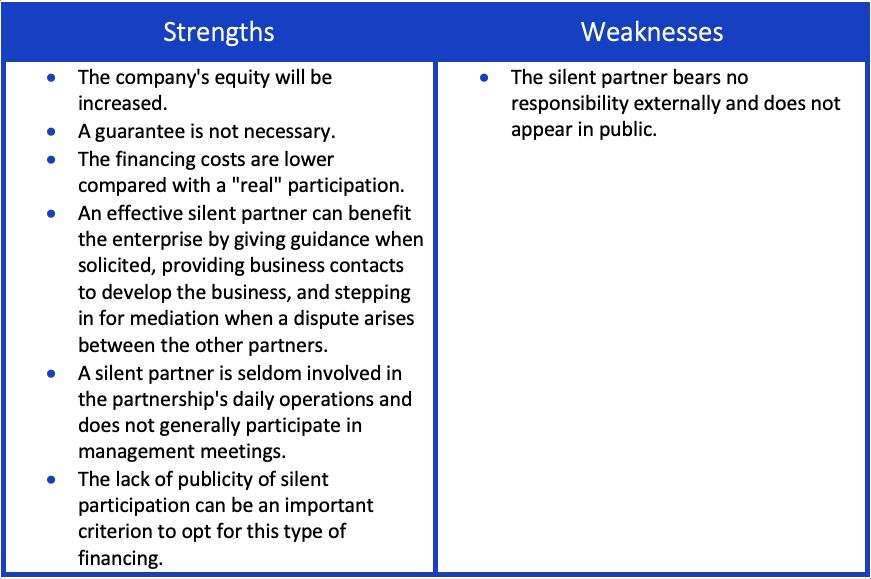

A silent partner is an individual whose involvement in a partnership is limited to providing capital to the business. A silent partner is also known as a limited partner, since his/her liability is typically limited to the amount invested in the partnership. In this form of financing one or more persons take an equity stake in a company, but without assuming any liability to the company’s creditors. The typical “silent” participation affects only the company’s internal affairs and is not apparent to outside observers.

Requirements:

A silent partnership generally calls for a formal agreement in writing. The capital contribution can consist of either money, in kind or services.

Things to remember:

The silent partner has the right to monitor the company’s business and can also be granted rights to be informed and to participate in the company’s decision making. However, the details of participation in profits or losses, involvement in the company’s management, supervision and information rights can be structured flexibly. As a case in point, usually the silent investor participates in losses up to their invested capital amount, but the parties may remove this feature partially or completely from the contract. It is considered a background role that cedes control to the general partner. Thus it requires the silent partner to have full confidence in the general partners' ability to grow the business. The silent partner may also need to ensure that their management styles or corporate vision are compatible.

•EU-wide application: Yes. As the requirements are lower compared with other forms of financing.

•Type (size) of SME business transfer: Medium-risk profiles, all forms of business transfers

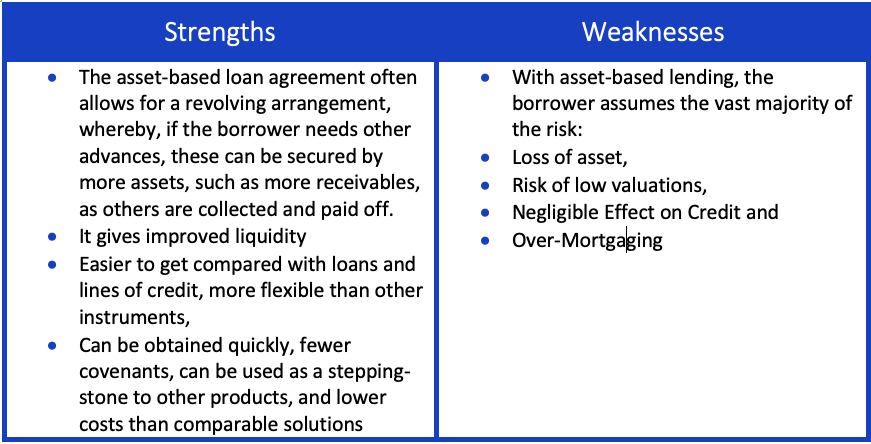

Asset-based lending (ABL) is any form of lending secured by an asset.

Typically, four types of asset classes are secured under ABL:

accounts receivable

inventory

equipment

real estate

Requirements:

The amount a firm can borrow depends on the appraised value of the selected assets, rather than on the overall creditworthiness of the firm, taking into account the ease to sell off the assets should the borrower be unable to generate cash to repay the loan. The amount of credit extended is linked to the liquidation value of the assets, which is estimated and monitored on the basis of hard data. Thus, monitoring and asset evaluation methodologies are of the utmost importance for this type of lending, which explains the historical use of ‘tangible’ assets to secure loans and, on the other hand, the limited exploitation of intangibles, such as trademarks, patents and copyright.

Things to remember:

In light of the above risks, particularly of the expected asset value dilution and losses, asset-based lenders typically lend at a discount to the actual value of the secured assets.

EU-wide application: It demands a sophisticated and efficient legal system.

Type (size) of SME business transfer: Low-risk profiles, financially small business transfers

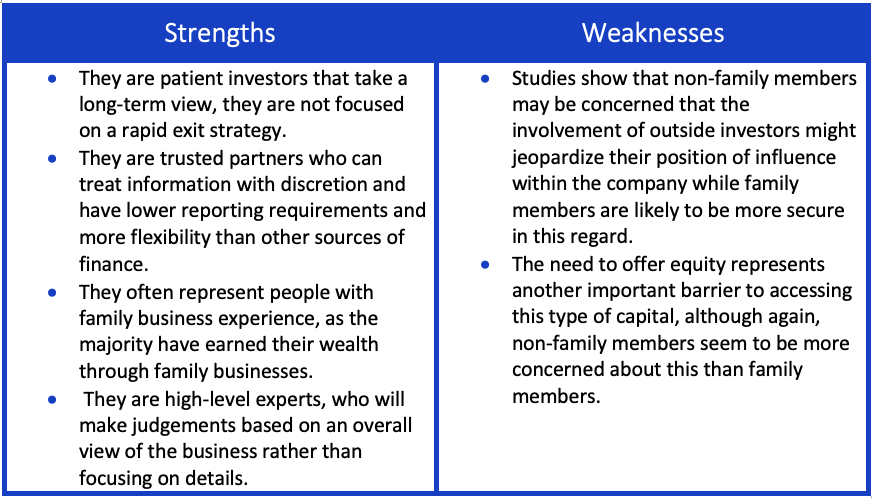

These individuals are looking for investments with reasonable risks and reasonable returns and are focused on long-term capital appreciation. Both of these traits are well matched by investing in family businesses.

Requirements:

These individuals are happy to be involved and offer their advice. They would often like to have an equity stake, which (in some cases) could be a barrier to investment.

Things to remember: The main factor that would deter HNWIs from investing in family businesses is the possibility of conflict among investee family members. Apart from this, the main reason given for not making more of these types of investments is a lack of availability and limited information on the opportunities.

EU-wide application: Needs an integrated and well-functioning financial system, a diffused culture for risk-taking and social recognition for an entrepreneurial career.

•Type (size) of SME business transfer: Medium-risk profiles, family succession